Zakah on Debts — What You Owe vs. What You're Owed (2026)

Zakat on debts depends on control: subtract short-term debts you owe, and include money owed to you only if you realistically expect to receive it. Understanding this distinction ensures you calculate zakat accurately without overpaying or missing what is due.

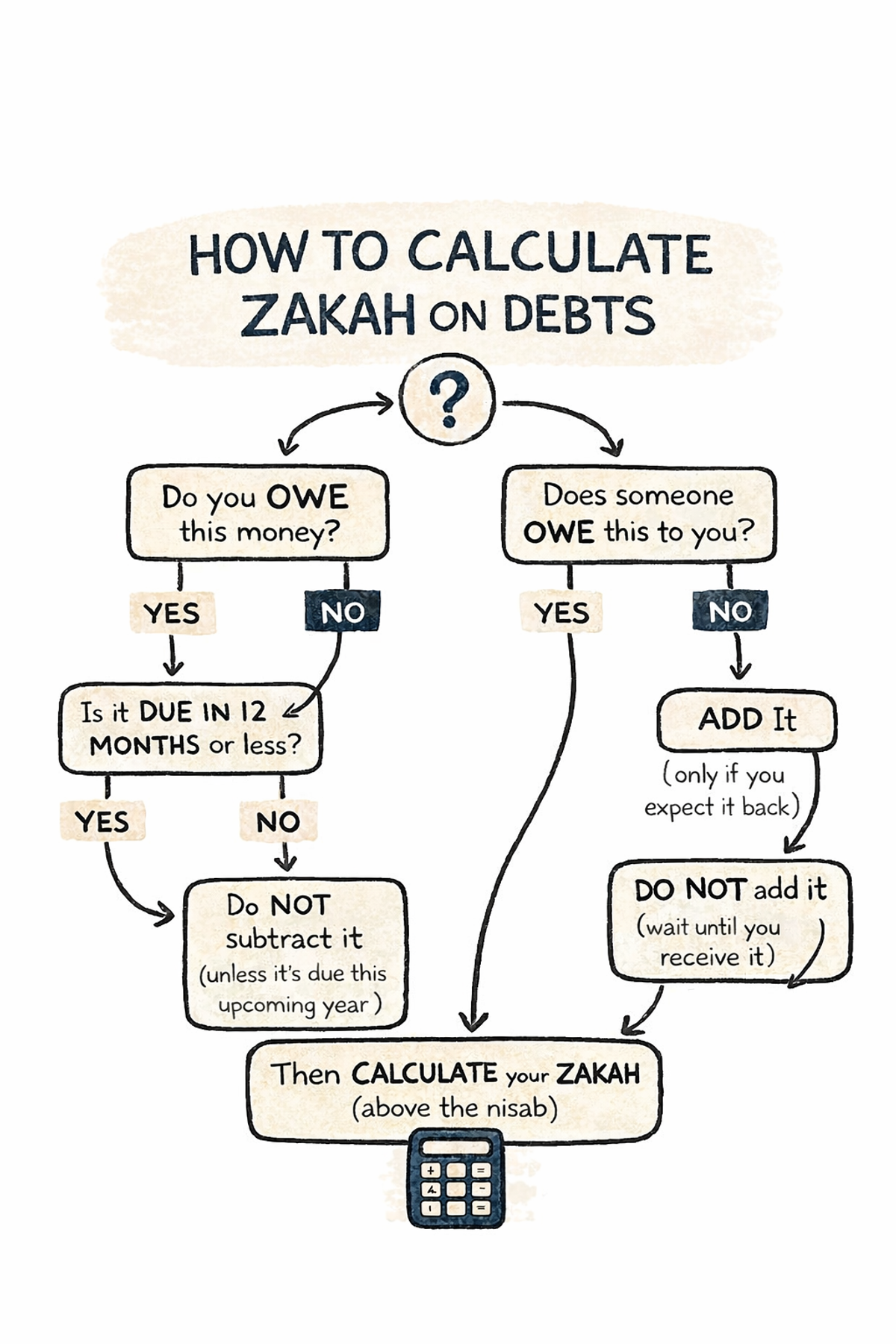

Zakah gets confusing the moment debt is involved.

Do you subtract what you owe?

Do you pay zakah on money someone owes you?

What if you’re not sure you’ll get it back?

This is where most people either overpay or delay unnecessarily.

Let’s make it simple and correct.

The Core Principle

Zakah is only due on wealth you actually own and can access.

Debt affects that in two ways:

- Money leaving your control (what you owe)

- Money not yet in your control (what you’re owed)

Understanding this difference is everything.

1. Zakah on Debts You Owe

If you owe money, it can reduce your zakahable wealth.

What You Can Deduct

You can subtract short-term debts due within the year, such as:

- Credit card balances

- Personal loans due soon

- Bills or payments you must pay now

These directly reduce what you own today.

What You Should Not Deduct

Long-term debts are different.

For example:

- Mortgages

- Student loans

- Long-term financing

You do not subtract the full amount.

Instead, only subtract:

- The amount due in the next 12 months

Simple Example

You have:

- $20,000 in savings

- $3,000 in short-term debt

Zakahable amount = $17,000

You pay zakah on what you actually have access to.

2. Zakah on Money Owed to You

This is where most people get stuck.

Not all debts owed to you are treated the same.

Case 1 — Strong Debt (You Expect Repayment)

If someone owes you money and you are confident you’ll get it back:

- You include it in your zakah calculation

- Even if you haven’t received it yet

Examples:

- Loan to a trusted friend

- Money owed by a stable business

- Formal agreements

Case 2 — Weak Debt (Uncertain or Delayed)

If repayment is unclear or unlikely:

- You do not pay zakah yearly

- You wait until you actually receive the money

Then:

- You pay zakah once on that amount

Examples:

- Someone avoiding payment

- Informal loans with no clarity

- Disputed or delayed money

3. The Mistake Most People Make

Two common issues:

- Over-deducting debt

People subtract their full mortgage or total loans - Ignoring money owed to them

Especially when it’s actually recoverable

Both lead to inaccurate zakah.

4. A Practical Way to Calculate

Keep it simple:

Step 1

Calculate everything you own:

- Cash

- Savings

- Gold

- Investments

- Business assets

Step 2

Subtract: Short-term debts (due within 12 months)

Step 3

Add: Money owed to you that you expect back

Step 4

Check if you are above the nisab

Step 5

Pay 2.5%

5. Why This Matters

Zakah is not just a calculation.

It’s an obligation tied to:

- Your wealth

- Your honesty

- Your accountability

Being careless with it isn’t a small issue. At the same time, overcomplicating it isn’t the goal. Clarity is.

Final Thought

Most people don’t struggle with zakah because it’s difficult.

They struggle because they’ve never seen it explained properly.

If your situation is complex, take the time to verify it properly.

If you have questions about your deen or want to make sure you're aligned, consider speaking to a qualified scholar or explore tools available at MeezanApp.com.